How Co Applicant Profiles Affect Education Loan Approval In India

Income, CIBIL Score, and Financial Stability: How Co-Applicants Decide Education Loan Approval in India

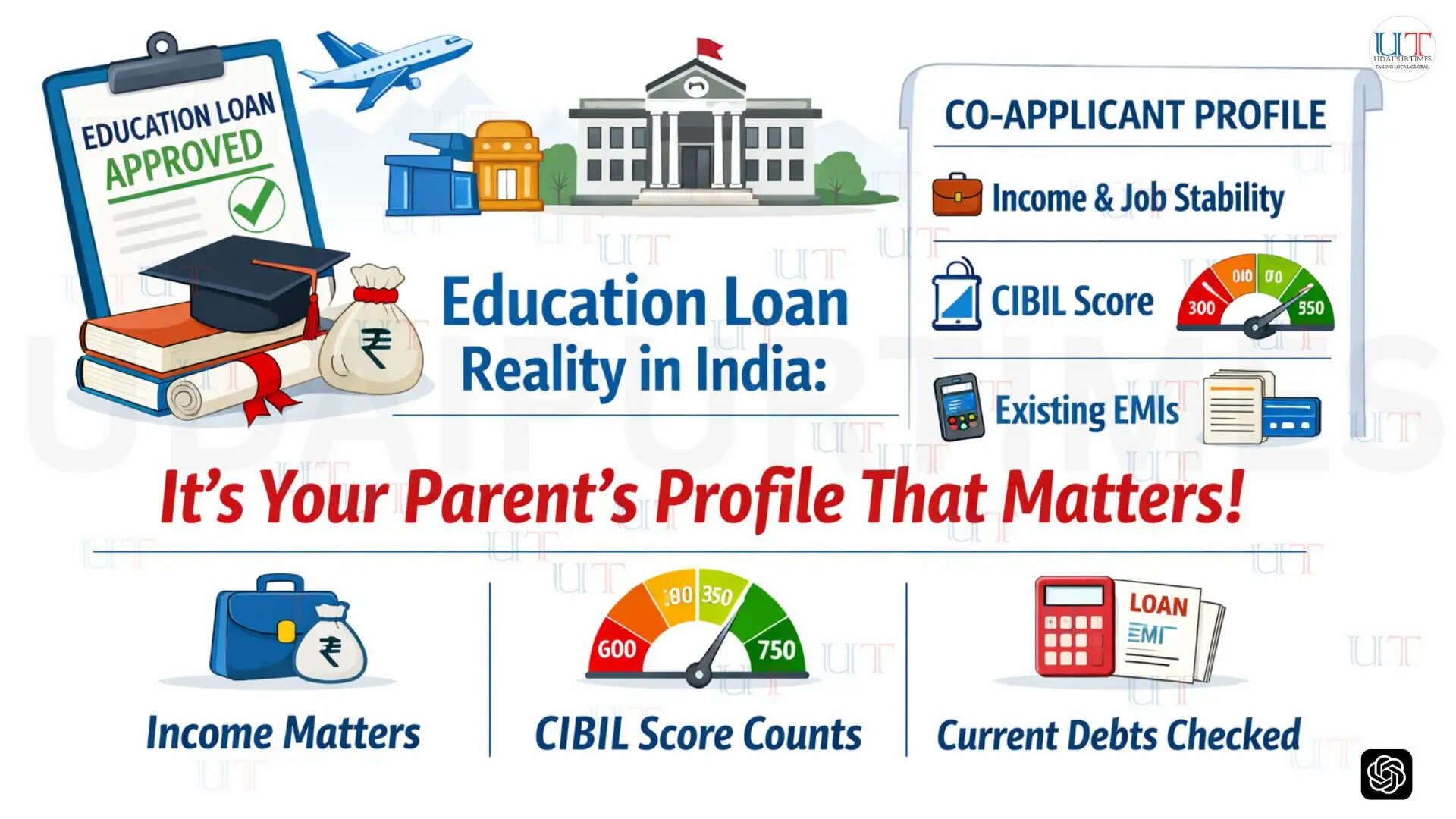

Why Banks Insist on a Co-Applicant

Indian banks treat education loans differently from other forms of credit. The borrower is typically someone with no income, no credit history, and no assets. A 19-year-old heading to college is, from a lender's perspective, a risk with no track record. The co-applicant fills that gap. They provide the financial credibility that the student simply cannot.

For most loans, especially those above ₹4 lakh for domestic studies or ₹7.5 lakh for education loan india programs involving overseas universities, a co-applicant is mandatory. Banks require this because the co-applicant becomes equally liable for repayment. If the student defaults, the bank turns to the co-applicant. This isn't a formality. It's the bank's primary safety net.

Income and Employment Stability

The co-applicant's income is the single most influential factor in the approval process. Banks want to see a stable, verifiable income that can cover EMIs if the student is unable to repay after the moratorium period ends. A salaried co-applicant working in government or a well-known private company will have an easier time than a self-employed individual with inconsistent earnings, even if the self-employed person earns more on paper.

The reason is predictability. Banks model their risk based on how confident they are that repayment will happen on schedule. A government employee with a modest salary of ₹50,000 per month often gets faster approval than a business owner earning ₹2 lakh monthly but with fluctuating returns. Tax filings, salary slips, and employment tenure all feed into this assessment. A co-applicant who has been in the same job for five or more years signals stability. Someone who has switched jobs three times in two years raises questions, regardless of their current salary.

Credit History and CIBIL Score

A co-applicant's CIBIL score can quietly kill a loan application. Most banks in India expect a score of 700 or above. Some are willing to work with 650, but the terms get worse: higher interest rates, lower sanctioned amounts, or demands for additional collateral.

What catches many families off guard is that the co-applicant's past financial behaviour is scrutinized in detail. Outstanding credit card balances, delayed EMI payments on a home or car loan, or being a guarantor on someone else's defaulted loan will all show up. Even settled accounts, where a borrower negotiated to pay less than the full amount owed, are treated as red flags. Banks interpret settlements as evidence that the person could not meet their original obligations.

If your parent has a clean credit history with timely repayments across all obligations, approval becomes smoother. If they don't, you'll need to address this before applying. Improving a CIBIL score takes time, often six months to a year of disciplined repayment behaviour.

Existing Debt Obligations

Banks assess the co-applicant's debt-to-income ratio with real scrutiny. If your parent already has a home loan EMI consuming 40% of their monthly income, adding an education loan EMI on top becomes a harder sell. Lenders generally prefer that total EMI obligations, including the proposed education loan, stay below 50% of the co-applicant's net monthly income.

This is where many applicants miscalculate. They look at the co-applicant's gross income and assume they'll qualify. But banks subtract existing liabilities first. The number that matters is how much room is left after all current obligations are met. This practical math is central to study loan eligibility, and overlooking it leads to avoidable rejections.

Age of the Co-Applicant

A co-applicant who is 55 years old and applying for a loan with a 15-year repayment tenure creates a problem. The bank knows that this person will likely retire before the loan is fully repaid. Retirement typically means reduced income, which increases the risk of default.

Younger co-applicants, or those with more working years left, are preferred. Some banks will approve a loan with an older co-applicant but may shorten the repayment window, which increases the EMI amount. Others may ask for a second co-applicant or additional security.

What Families Can Do

Planning the co-applicant's profile should start well before the loan application. Check the co-applicant's CIBIL report early, clear any small outstanding debts, and ensure tax returns are filed and up to date. If the obvious co-applicant has a weak profile, consider whether another family member with stronger credentials can step in.

The student's merit gets them into the university. The co-applicant's financial profile gets them the loan. Treating both with equal seriousness is the only practical approach.